Claim Tax Treaty, Avoid Double Taxation and Request VAT Exemption – Form 6166 – Certification of U.S. Tax Residency

Form 6166 is your key to ensuring that you are taxed fairly in a foreign country, and in most cases avoid double taxation, or mandatory withholding on payment transferred from an overseas vendor or payor.

What is Form 6166?

Form 6166 is also known as Certification of Tax Residency —and it’s just what that sounds like. Form 6166 certifies that, for tax purposes, you are a resident of the United States. Why is that significant? We’ll get to that in a moment. First, let me introduce you to Form 8802.

What is Form 8802?

Form 8802 is what you have to fill out when you apply for a Form 6166 Certification of Tax Residency. You can find Form 8802 on the IRS website.

Why does any of this matter?

When you earn income for services or sell goods in a foreign country, that country may require the payor to withhold taxes based on the foreign country’s own tax codes. Because of U.S. treaties, however, tax residents of the U.S. qualify for reduced tax rates or may be exempt from tax in many foreign countries. The Form 6166 Certification of Tax Residency is how you prove to a foreign country that you qualify for those treaty benefits.

So, what are those treaty benefits, exactly

Well, that varies from country to country. But in addition to receiving a reduced tax rate or tax exemption, many foreign countries also exempt you from VAT (Value Added Tax). As you can see, Form 6166 is a priceless tool in reducing your foreign taxes and keeping more money in your pocket. It is really worth it

Let’s get down to the nitty-gritty…

In order to qualify for your Form 6166, you have to file a U.S. Tax Return in most cases for the year you are claiming residency, (And your tax return cannot be filed as a Non-Resident Tax Return.)

Form 6166 (Certification of Tax Residency) only lasts for one year, so you will have to apply annually. The IRS recommends that you send in your Form 8802 at least 45 days before you need Form 6166. We recommend that you apply even earlier than that.

CAUTION: The usual timeline for processing these forms used to be 45 days, but the coronavirus pandemic has created significant delays at the IRS. Expect your certification to be approved within 90 days after submission. There is also potential for significant delays beyond the 90 days if you failed to accurately complete the 8802 forms.

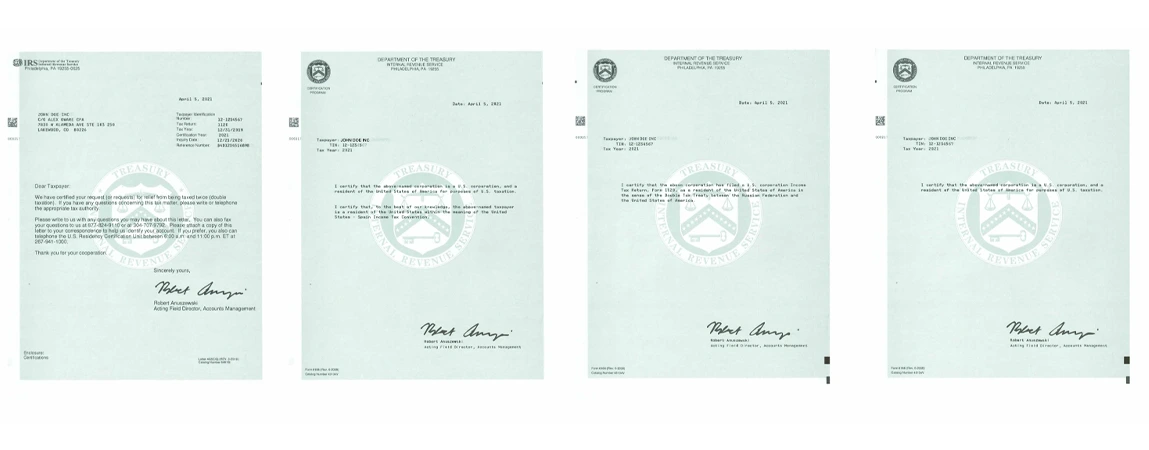

If all certification requirements are met, the proper U.S. Residency Certification will be issued on Form 6166, Certification Program Letterhead. Click here to see samples of Tax Year 2021 certifications

U.S Residency Certification for Domestic and Foreign Partnerships, including U.S Multiple Member LLCs …

A partnership organized in the United States, and other countries, may obtain a certificate of residency on Form 6166 on behalf of its partners, by submitting a request for certification on Form 8802 to the IRS. Generally, domestic partnerships and foreign partnerships with U.S. source income, are required to file Form 1065. The Form 6166 will confirm the filing of such form and includes the names of all partners who have filed tax returns as U.S. residents.

On the form 6166, IRS will inform the withholding agent to contact the partnership directly to provide information regarding the allocation of the specific foreign country’s source income to the listed U.S. partner. If a foreign partnership with U.S. partners is not required to file a Form 1065, the Form 6166 will confirm that position and otherwise contain the same information regarding its U.S. partners.

U.S Residency Certification for S Corporations …

An S corporation may submit a Form 8802 and obtain a Form 6166 certificate of residence in a manner similar to that of a partnership as explained above. A Form 6166 confirms the filing of an information return, Form 1120S, as required for an S corporation, and includes a list of shareholders who filed returns as U.S. residents.

U.S Residency Certification For U.S Owned Single Member LLCs …

A U.S. resident that is a single member owner of an LLC or other entity that is disregarded as an entity separate from its owner for U.S. tax purposes may submit a Form 8802 to obtain a Form 6166 that provides that the LLC or other entity is a branch, division or business unit of its single member owner and that such single member has filed a tax return as a resident of the United States.

U.S Residency Certification For Foreign Owned U.S Single Member LLCs …

A foreign or U.S owned single-member LLC that is disregarded as an entity separate from its owner is not a U.S “person”, and is also not “liable to tax”. IRS will not certify that the LLC is a resident of the United States. However, the IRS may certify that the single owner of the LLC is a resident of the United States.

The IRS released the IRS released International Technical Assistance (ITA), which clarified that a single-owner LLC is a disregarded entity separate from its owner for federal income tax purposes, the LLC is not a person for purposes of U.S income tax treaties. The IRS further stated that the income of the single-owner LLC is taxable in the hands of the single owner, and not in the hands of the LLC. The LLC is not liable to tax within the meaning of U.S income tax treaties, and even under the domestic law. Therefore an LLC owned by a foreign person cannot certify that the LLC is a resident of the United States.

A foreign owned single member LLC as the name suggests is any single member LLC owned by a person who is not a U.S resident. i.e. Non-Resident Alien. Therefore a non-resident alien cannot certify either his single member LLC or himself as a U.S resident. Residency within the meaning of the various tax treaty provisions are generally determined by reason of a person or company’s domicile, residence, citizenship, place of management, place of incorporation, or any other criterion of a similar nature.

If you need specific treaty details for specific countries, you can find these posted on the IRS website. Or, feel free to contact us. We’re here to help! This is obviously only a quick look at the 6166 and 8802 forms.

There is a lot more to this—and that’s why we’re here. We would love to help you navigate the complexities of Form 6166, from identifying how many copies of Form 6166 you need to expediting your applications on future years. Just get in touch with us and let us know about any questions you have. We look forward to helping you! Let’s talk.

If you’re in need of professional bookkeeping services, we recommend visiting our subsidiary, URSA Services LLC. They specialize in keeping your finances in order so you can focus on growing your business. Don’t worry, we’ll still be here to handle all your tax needs. Visit URSA Services LLC today to learn more!!

Related Articles:

- How to File Forms 5472 and 1120 for a Foreign-Owned Single Member LLC

- USA – INDIA F-1 & J-1 Tax Treaty (Students & Business Apprentice)

- What Forms Do Foreign-Owned Single Member LLCs Have to File?

- 7 Common Questions about Foreign-Owned U.S. LLCs Answered—by a CPA

- Amazon Foreign Sellers, US Taxation and 1099-K Reporting

- The 12 Most Important Questions about U.S. LLCs Answered—by a CPA

- Samples of U.S. Residency Certifications – Form 6166

- 15 Common Questions About Expatriation, Form 8854, and the Exit Tax—Answered by a CPA

- Forms and Filing for Foreign-Owned LLC Multi-Member Partnerships | Exploring a Case from an Australian-Owned U.S. Partnership

- Which Tax Forms Do Foreign-Owned U.S. Multi-Member LLCs Have to File?

WATCH – C-Corporation: Applying for 2023 U.S Residency Certification Form 8802/6166

WATCH – C-Corporation: Applying for 2023 U.S Residency Certification Form 8802/6166Book a paid consultation

Yes, Book My Slot

***Disclaimer: This communication is not intended as tax advice, and no tax accountant/Attorney client relationship results**